Canada-US labour competitiveness: Details matter

Canada needs to think small. We need to do give much more thought to proposals to boost investment capital toward small and medium-sized firms

We have hit that point in the cycle where the flurry of reports on the challenges facing the Canadian economy emerge. A regular period of navel gazing.

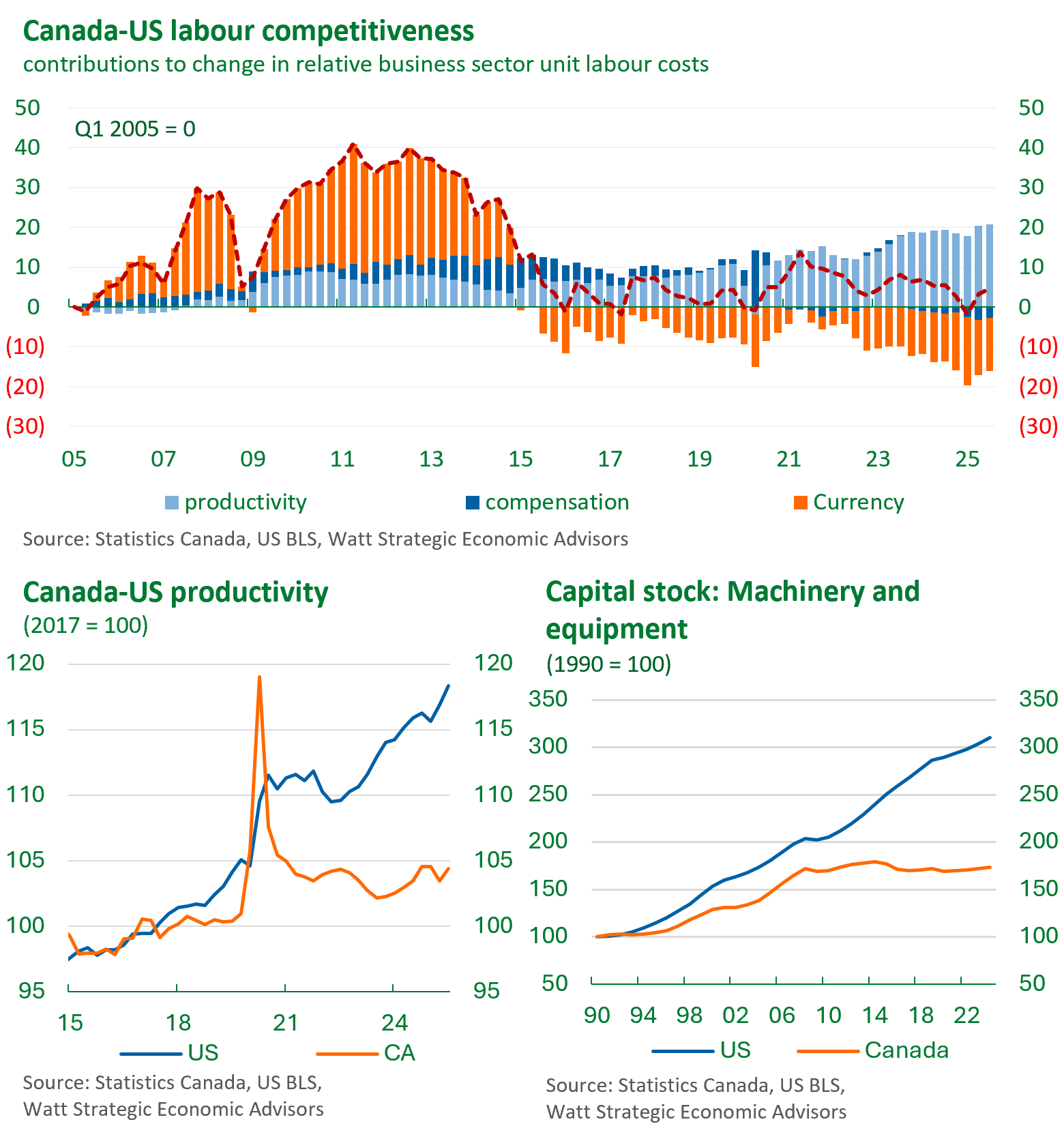

In such circumstances, we like to post an update of the top chart. It shows the relative change in Canada and US unit labour costs since Q1 2005. There might be better representations, but this version is revealing.

I’ve updated this chart every quarter since roughly 2012. Back then, Canada had labour competitiveness disadvantage. It was partly due to lagging productivity growth relative to the US, a small divergence in compensation trends, but the bulk of the gap was due to the strong Canadian dollar in the wake of the commodity super cycle.

At the time, USD/CAD was lingering around parity.

Over the next few years, the gap narrowed. The Canadian dollar weakened and Canadian labour productivity outperformed modestly.

In 2014/2015, things changed. Oil prices collapsed and the Canadian dollar weakened shifting from a labour competitiveness headwind to a tailwind.

Then, the labour productivity gap began to widen with the US outperforming. This has continued for the past decade.

Looking at the relative ULC measure right now, there does not seem to be much of a gap. Relative unit labour costs don’t seem much changed relative to 2005. There does not seem to be much of a labour cost competitiveness gap.

Details matter

That “neutral” labour cost competitiveness backdrop actually reflects a huge US labour productivity outperformance that is largely offset by Canadian dollar weakness. That is not a good trade-off for Canada.

If Canada wants to improve our labour cost competitiveness, we could boost productivity growth to a trajectory that closes the gap with the US. That would be the preferable situation. However, boosting productivity is hard and Canada, honestly, is out of practice in that regard.

Maybe there are easier solutions.

The chart suggests two:

All Canadians can accept a substantial cut in their compensation. This might well have to include those that were eager to cheer PMMC in Davos as the pain must be spread around.

Actively push the Canadian dollar down even further.

The second chart presents the stark divergence in Canada-US labour productivity in recent years. Even more worrisome from a Canadian perspective is that US labour productivity growth seems to be accelerating. Hence, the US has a large lead and they are dropping the hammer.

It seems that the US might be in an economic cycle featuring sustained higher productivity growth. I would contend that erratic policymaking puts that at risk, but it is still a very good story helping provide underlying resilience to the US economy.

In a discussion of US productivity, two economists at the Federal Reserve Bank of Dallas wrote about AI’s role in productivity growth (see “Advances in AI will boost productivity, living standards over time“ Mark A Wynne and Lillian Derr, 24 June 2025).

There are actually a lot of research reports on this topic. I cite this one because of this because of this paragraph:

“Artificial intelligence (AI), like many technologies before it, offers the potential to improve people’s living standards. Such advances can be approximated by changes in gross domestic product (GDP) per capita over time—the rate of change in the amount of output per person.”

This hits home for two reasons. First, Canada’s AI adoption has been lacklustre and second, Canada’s per capita GDP growth has been distressing. This has been the case even as population growth has slowed sharply. Unfortunately, GDP growth also slowed sharply.

It is hard to overlook or disentangle Canada’s lagging productivity performance vis-a-vis the US, and the divergent trends in machinery and equipment net capital stocks as shown in the third chart. In the US, the M&E capital stock has been on a steady, solid upward trajectory. Canada’s has been effectively flat since 2008. (Keep in mind that it was the US that was hammered by the 2008/09 global financial crisis. Canada emerged largely unscathed, but it seems that it was Canadian enthusiasm to invest in M&E that was crushed.)

Catching the US seems unrealistic, but Canada seems to need to do something to try to close the gap a bit. It is possible that the US will stumble on its own due to policy missteps that might make the US a less attractive investment destination, but a better strategy is to try to control your own circumstances.

Sweat small stuff: Act local in order to think global

We have proposed before that while the Federal Government is focused on BIG things, large projects, ones that get headlines and photo ops, they (and other levels of government) need to think, and act, on smaller scale issues.

In June 2025, we highlighted the need to sweat the small stuff (Build big things, but also sweat the small stuff, 4 June 2025) That is give more thought (and policy focus at all levels of government) on improving the investment environment for smaller firms.

“ … amid the focus on major projects, we also need to think small. Canada desperately needs to boost investment in machinery and equipment. Hopefully, this will happen as spillover from major project investment. However, it will also require a regulatory backdrop conducive to investment — reducing red-tape and speeding up the process of bringing factories online among other factors that will require co-operation among all levels of government.”

We need to improve the incentives for those with capital to boost investment in those (Canadian) firms that might not have size now, but have the potential to be world beaters.

David Watt | Watt Strategic Economic Advisors

LinkedIn: www.linkedin.com/in/david-g-watt